Subscription Billing Math: MRR, ARR, Churn, LTV Explained

A plain-English guide to SaaS billing math for non-finance founders: how to calculate MRR, ARR, churn, and LTV, with worked examples and 2026 benchmarks.

· Justin Boggs

Photo by Jakub Żerdzicki on Unsplash

Subscription billing math comes down to four numbers, and you can learn all of them in an afternoon. MRR is the recurring revenue you collect in a month. ARR is that number annualized — usually just MRR times twelve. Churn is the fraction of customers or revenue you lose in a period. LTV is the total revenue you expect from an average customer before they leave. None of these require finance training. They require arithmetic and the discipline to define your terms once and stick to them. This guide walks through each formula with a worked example, gives you the current benchmarks, and tells you which numbers actually change what you do on Monday.

TL;DR

- MRR = active subscribers × average revenue per user. Count only recurring revenue, never one-time charges.

- ARR = MRR × 12 for monthly-billing SaaS. It's an annualized run rate, not a guarantee.

- Churn compounds. 5% monthly churn loses roughly 46% of a cohort in a year.

- LTV = average revenue per account × gross margin ÷ churn rate. Compare it to your cost to acquire a customer.

- The one ratio worth watching long-term is LTV:CAC; a healthy SaaS target is about 3:1, per Wall Street Prep.

What MRR actually is (and what it isn't)

Monthly Recurring Revenue is the predictable, recurring revenue your active subscriptions generate in a single month. The word that does all the work in that sentence is recurring. A one-time setup fee, a consulting hour, a one-off Pro upgrade that doesn't renew — none of those belong in MRR. They're real money, but they're not recurring, so mixing them in pollutes the one number that's supposed to be predictable.

The simplest way to calculate MRR is subscribers times average revenue per user (ARPU):

MRR = number of active subscribers × average revenue per user.

Say you run two plans. You have 90 customers on a $79/month plan and 60 customers on a $149/month plan. Your MRR is (90 × $79) + (60 × $149) = $7,110 + $8,940 = $16,050. That's it. No spreadsheet gymnastics required.

The trap most first-time founders fall into is annual plans. If a customer pays $948 upfront for a year, that is not $948 of MRR in the month they paid. It's $79 of MRR for each of the next twelve months. You normalize annual contracts back to a monthly figure so your MRR line doesn't spike every January and crater every other month. The whole point of MRR is a smooth, comparable signal — lumpy annual payments defeat that.

It also helps to break MRR into its moving parts: new MRR from fresh customers, expansion MRR from upgrades, contraction MRR from downgrades, and churned MRR from cancellations. Net new MRR for the month is new plus expansion minus contraction minus churn. When your MRR is flat, this breakdown tells you whether you're stalled or whether you're acquiring fast and leaking just as fast — two very different problems with two different fixes. If you've never set up the analytics to capture these events, the same instrumentation that tracks signups handles it; I covered the plumbing in the first-month SaaS dashboard.

ARR: the number investors ask about

ARR is where the confusion starts, because the acronym means two different things. As ChartMogul lays out, ARR can stand for Annual Recurring Revenue or Annualized Run Rate, and they're calculated differently.

For most modern indie SaaS — the kind billed mostly month-to-month — the one you want is Annualized Run Rate, and the formula is gloriously simple:

ARR = MRR × 12.

Using the example above, $16,050 of MRR is $192,600 of ARR. You're not promising you'll collect every dollar of that; you're saying "at today's run rate, this is the annual pace." ChartMogul's own CEO frames it bluntly: in their app, ARR is defined as Annualized Run Rate, MRR × 12, because that's "the most popular meaning of ARR, and the most broadly useful one today."

Annual Recurring Revenue, the stricter definition, only counts contracts of a year or longer, and it's calculated as total contract value divided by the number of years. A four-year, $6,000 contract is $1,500 of Annual Recurring Revenue. This version matters if most of your revenue comes from annual or multi-year deals. For a solo founder selling monthly subscriptions, it mostly doesn't — and ChartMogul notes this strict definition has become "almost meaningless" for the mostly-monthly companies that launched in the last several years.

Two things ARR never includes: one-time payments and professional-services revenue. Folding those in is how transactional businesses with no subscriptions at all dress up a good month as "ARR" by multiplying it by twelve. Don't do that to yourself — you'll make planning decisions against a number that isn't real.

Why bother annualizing at all? Because $16,050 of MRR is hard to reason about, while "$193K ARR" is a number you can plan a year around. It's the unit founders, boards, and acquirers all speak. Just state which definition you're using and you'll avoid the most common reporting mistake in SaaS.

Why churn is the number that compounds

Churn is the rate at which you lose customers or revenue in a period, and it's the most important number on this page because it compounds against you. I wrote a full breakdown in churn analysis for non-tech founders, but the billing-math version is short.

There are two churns and you need both. Customer churn = customers lost ÷ customers at the start of the period. Revenue churn weights that by dollars. Lose one $500/month account out of a hundred customers and your customer churn is 1% while your revenue churn might be 5% — the gap is the lesson. When they disagree, believe revenue churn.

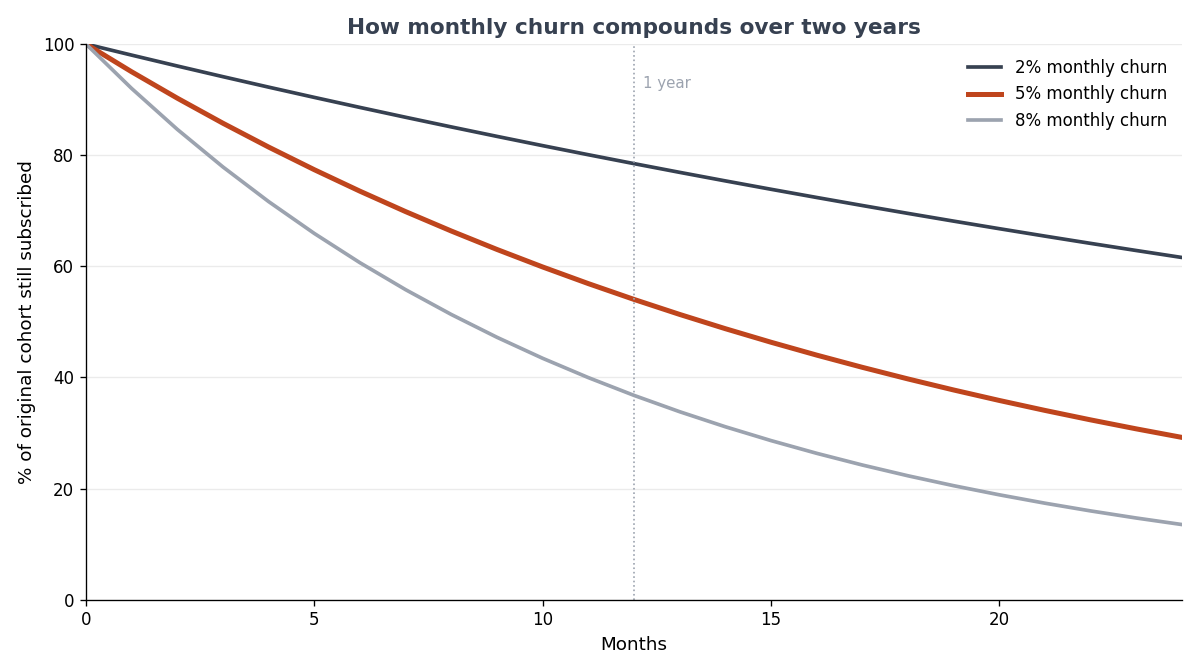

Here's the part that blindsides founders. A 5% monthly churn rate sounds survivable. Run the compounding and it isn't: 0.95 to the twelfth power is about 0.54, meaning you lose roughly 46% of a cohort over a year. The chart below shows three churn rates playing out across two years.

At 2% monthly churn, more than three-quarters of a cohort is still around after a year. At 8%, you've lost nearly two-thirds. Same product, wildly different businesses — and the only variable is a few percentage points of monthly churn. This is why early-stage founders who ignore churn get ambushed twelve months in: the damage is invisible month to month and brutal in aggregate.

For context on what's normal, ChartMogul's benchmark data, drawn from more than 2,500 SaaS businesses, puts median monthly customer churn for early-stage companies (under $300k ARR) at about 6.5%. It falls as you grow and tighten your ideal customer. If you're well above that and small, fixing churn beats spending on acquisition every time — you're pouring water into a bucket with a hole in it.

LTV: what a customer is worth

Customer Lifetime Value is the total gross-margin revenue you expect from an average customer before they churn. It answers the question every acquisition decision hinges on: how much can I afford to spend to land a customer?

The standard formula, per Wall Street Prep, is:

LTV = average revenue per account × gross margin % ÷ churn rate.

The churn rate in the denominator is doing something clever: dividing by churn is the same as multiplying by the average customer lifetime. If 5% of customers leave each month, the average customer stays about 20 months (1 ÷ 0.05). So a customer paying $79/month at an 85% gross margin, churning at 5% monthly, is worth roughly $79 × 0.85 ÷ 0.05 = about $1,343 in lifetime gross profit.

Two notes that keep this honest. First, use gross margin, not revenue — a dollar of subscription revenue costs you something in hosting, payment fees, and support, and LTV should reflect profit, not top line. Second, LTV is only meaningful next to CAC, your customer acquisition cost: total sales and marketing spend divided by new customers acquired. LTV alone tells you nothing about whether the business works.

The ratio of the two is the number to watch. A healthy SaaS LTV:CAC ratio is around 3:1 — you earn three dollars of lifetime value for every dollar spent acquiring a customer. Wall Street Prep flags below 1:1 as unsustainable (you lose money on every customer) and notes that a very high ratio like 5:1, while profitable, can mean you're underinvesting in growth and leaving the market to competitors.

Here's how the four numbers stack up for our running example:

| Metric | Formula | Worked value | | --- | --- | --- | | MRR | subscribers × ARPU | $16,050 | | ARR | MRR × 12 | $192,600 | | Customer churn | lost ÷ starting customers | 5% / month | | Avg. customer lifetime | 1 ÷ churn | ~20 months | | LTV (per $79 customer) | ARPU × margin ÷ churn | ~$1,343 | | Healthy CAC ceiling | LTV ÷ 3 | ~$448 |

Read the last row carefully: it says you can spend up to about $448 to acquire a $79/month customer and still hit a 3:1 ratio. That single number turns "is this marketing channel worth it?" from a gut call into arithmetic.

Net revenue retention: the number that beats acquisition

Once you understand MRR, churn, and expansion, one combined metric tells you whether the business grows on its own: net revenue retention (NRR). It measures how much recurring revenue you keep from an existing cohort over a period, after expansion, contraction, and churn — but excluding any new customers.

The formula is the starting MRR of a cohort, plus expansion, minus contraction, minus churn, all divided by the starting MRR:

NRR = (starting MRR + expansion − contraction − churn) ÷ starting MRR.

Say a cohort starts the year at $10,000 of MRR. Over twelve months, upgrades add $2,000, downgrades remove $500, and cancellations remove $1,000. Your ending MRR from that same cohort is $10,500, so NRR is $10,500 ÷ $10,000 = 105%. That number above 100% is the holy grail: it means the cohort grew even though some customers left and you added zero new ones. Expansion from your happiest customers more than covered the revenue you lost to churn.

This is why expansion revenue matters so much, and why so many maturing SaaS companies shift focus from pure acquisition toward growing revenue per account. ChartMogul's case study of Buffer is the textbook version — they hit $20M ARR not by endlessly chasing new signups but by growing average revenue per account among existing users, because their own metrics showed that further growth on customer count alone would be a grind.

For an indie founder, NRR below 100% means you're on a treadmill: every month starts with a hole you have to fill with new customers just to stay flat. NRR above 100% means the treadmill runs in your favor — even a slow month of acquisition still nets out positive. You probably won't have a clean NRR figure with your first ten customers, but it's the number to grow into, and pricing tiers that give happy customers room to spend more are how you get there.

Putting the numbers to work

Metrics you don't act on are just anxiety with extra steps. Here's the short version of what each number should change.

MRR tells you the trajectory. Watch net new MRR — new plus expansion minus contraction minus churn. If it's positive and growing, keep doing what you're doing. If it's flat, the breakdown tells you whether to fix acquisition or retention.

ARR is your planning and conversation unit. Use it to set annual goals and to talk to anyone outside the business. Don't make operational decisions off it; it's a lagging, smoothed view.

Churn is your early-warning system. Track it monthly, separate voluntary (people who chose to leave) from involuntary (failed credit cards — a simple dunning email recovers much of this), and treat any spike as the most urgent thing on your plate. Retention compounds in your favor exactly as hard as churn compounds against you.

LTV:CAC is your growth governor. Below 3:1 and small, fix the product or your targeting before you spend more on ads. Comfortably above 3:1, you have room to spend faster. Pricing changes move both LTV and churn at once, which is why getting price right early matters so much — I went deep on that in SaaS pricing for non-tech founders.

One caution for very early founders: with ten customers, your churn rate swings wildly when one person leaves, and your LTV is a guess. Small-sample noise is real. Track the numbers from day one to build the habit, but don't over-steer on a single bad month until you have enough customers for the averages to mean something.

Frequently asked questions

What's the difference between MRR and ARR?

MRR is monthly recurring revenue; ARR is that number annualized, usually MRR × 12. MRR gives you a fast, month-to-month operational signal, while ARR is the smoothed annual figure you use for planning and for talking to investors or acquirers. They measure the same revenue at different time scales.

Does MRR include one-time payments or setup fees?

No. MRR counts only recurring subscription revenue. One-time charges, setup fees, and professional-services revenue are excluded because they aren't predictable month to month, and folding them in distorts the one metric that's supposed to be stable, per ChartMogul.

How do I count an annual subscription in MRR?

Normalize it to a monthly figure. A $948 annual plan contributes $79 of MRR in each of the twelve months it covers, not $948 in the month it was paid. This keeps your MRR line smooth and comparable instead of spiking whenever an annual customer renews.

What is a good LTV:CAC ratio for an indie SaaS?

About 3:1 is the common healthy target — three dollars of lifetime value per dollar of acquisition cost, per Wall Street Prep. Below 1:1 you lose money on every customer. Very early companies often run lower while finding product-market fit, and a ratio far above 3:1 can signal you're underinvesting in growth.

What churn rate should I expect early on?

Higher than you'd like. ChartMogul's benchmarks put median monthly customer churn for companies under $300k ARR around 6.5%, declining as you grow and refine your ideal customer. Early churn is noisy with a small customer base, so watch the trend rather than any single month.

Do I need special software to track these?

Not at first. A spreadsheet handles MRR, ARR, churn, and LTV for your first few dozen customers. Tools like ChartMogul or your analytics stack become worth it once the manual math gets tedious and you want automatic cohort and expansion tracking.

The math is the easy part

The reassuring thing about subscription billing math is that there's no advanced finance hiding in it. MRR is multiplication. ARR is multiplication. Churn is division. LTV is the two combined. Define each term once, count only recurring revenue, and you can run your whole business off four numbers and a spreadsheet.

The hard part isn't the arithmetic — it's the discipline to look at the numbers honestly every month and act on what they say, especially when churn is quietly compounding and the monthly view looks fine.

If you're building a SaaS with AI coding tools and want the billing plumbing already wired up correctly, Coding Capybaras is the free boilerplate I built for exactly this workflow — Stripe subscriptions, webhooks, and the event tracking behind these metrics ship in the box.